Note

Go to the end to download the full example code.

Getting Started with Optimal Unit Averaging¶

This tutorial walks you through the complete workflow of unit_averaging.

It lays out a template for going from raw data to optimal estimation with unit

averaging. Throughout, we use a real-world example: forecasting Frankfurt’s

unemployment rate using data from 150 German regions, while taking into account

the differences in regional dynamics.

By the end, you should be able to:

Define a focus function to map model parameters to your target (e.g., a forecast),

Prepare data on unit-level estimates.

Define and fit an optimal unit averager.

Compare results against the baseline of no averaging.

Functionality covered

OptimalUnitAverager, IndividualUnitAverager, and InlineFocusFunction

import numpy as np

import pandas as pd

from docs_utils import plot_germany

from statsmodels.tsa.ar_model import AutoReg

from unit_averaging import (

IndividualUnitAverager,

InlineFocusFunction,

OptimalUnitAverager,

)

Following along

If you would like to follow along on a local machine, please download the

contents of the data folder

here

. To recreate the plots, also download the docs_utils.py

file

.

Problem, Key Idea, Data¶

Introduction¶

Suppose that it is December, 2019 and we want to optimally forecast the change in the unemployment rate in Frankfurt in the next month. At our disposal we have a panel (longitudinal) dataset of unemployment rates for all the regions of Germany, Frankfurt included.

What is the key challenge to using all this data efficiently? The regions are different in unseen ways (or heterogeneous): each of them has its own unemployment dynamics, driven by differences in their economies, populations, and laws. Throwing the data on all the regions into a single prediction model usually may yield a very biased forecast for Frankfurt (or for any other specific region).

Unit averaging is ensemble method specifically designed for efficient estimation of such unit-specific target parameters (e.g. unemployment in Frankfurt) in settings with data on multiple units. It is applicable both with panel data, as in this example, and in meta-analysis settings.

Essentially, unit averaging computes a weighted linear combination of the estimates of all the units. By borrowing strength from similar units, optimal unit averaging reduces variance in estimates while controlling the bias caused by using units with different dynamics.

Data¶

To illustrate optimal unit averaging, we use data on the 150 German employment regions. The data records the unemployment rates for each region for each month between January 2011 and December 2019. It can be freely obtained from the German Federal Employment Agency.

A quick peek at the data, after reading it in and setting up the time index:

german_data = pd.read_csv(

"data/tutorial_data.csv", parse_dates=True, index_col="period"

)

german_data.index = pd.DatetimeIndex(german_data.index.values, freq="MS")

print(german_data.iloc[-4:, [0, 2, -1]])

Aachen - Düren Ahlen - Münster Deutschland

2019-09-01 6.2 4.6 4.9

2019-10-01 6.1 4.4 4.8

2019-11-01 6.0 4.5 4.8

2019-12-01 6.1 4.5 4.9

The different regions are identified by their string names, which serve as column names in the data:

regions = german_data.columns[:-1].to_numpy()

print(regions[:10])

['Aachen - Düren' 'Aalen' 'Ahlen - Münster' 'Annaberg-Buchholz'

'Ansbach - Weißenburg' 'Aschaffenburg' 'Augsburg' 'Bad Homburg'

'Bad Kreuznach' 'Bad Oldesloe']

Constructing Averaging Inputs¶

In short, every use of unit averaging involves the following steps:

Prepare the models:

Define a model for each unit.

Express the parameter of interest in terms of the parameters of the unit- level models (defining a suitable focus function)

Estimate the model for each unit separately and collect the results.

Pass the unit-level estimates, the focus function, along with any other necessary inputs to a suitable

Averagerfrom this package andfit()it.

See also

See this page for a more formal discussion of unit averaging from a mathematical perspective.

Region-Specific Models¶

In our case, we will specify that the change in unemployment in each region \(i\) follows a simple autoregressive (ARx) process: it depends on the unemploymentin the same region in the previous month, along with Germany-wide unemployment in the previous month:

where \(\Delta U_{i, t}\) is the change in the unemployment rate in region \(i\) in month \(t\).

While the general shape of the model is the same for all regions, the coefficients are region-specific. That allows different regions to have different unemployment dynamics.

Estimating Unit Models¶

The first key required input for all averagers is the information on the

estimated unit-level parameters (in this case the estimated

\(c_i, \alpha_i, \beta_i\)). In case of OptimalUnitAverager we need to

supply both the individual estimates and the associated unit-level estimated

covariance matrices of estimators.

All unit averagers accept data in two forms: as numpy arrays of arrays of estimates (and covariances, when appropriate), and dicts of estimates and covariances. Dicts are appropriate when the individual units have descriptive identifier, as in our case.

We initialize empty dicts for individual estimates and covariances:

ind_estimates = {}

ind_covar_ests = {}

We now estimate the coefficients \(c_i, \alpha_i, \beta_i\) unit-by-unit

by running a suitable autoregression with statsmodels. In line with the

above model, we estimate the model in differences:

# Difference data and create lag of Germany-wide rate

german_data = german_data.diff()

german_data["Germany_lag"] = german_data["Deutschland"].shift(1)

german_data = german_data.iloc[2:,]

# Iterate through regions

for region in regions:

# Extract data and add lags

ind_data = german_data.loc[:, [region, "Germany_lag"]]

# Run an ARx(1) model

ar_results = (

AutoReg(ind_data.loc[:, region], 1, exog=ind_data["Germany_lag"])

).fit(cov_type="HAC", cov_kwds={"maxlags": 5})

# Add to dictionaries

ind_estimates[region] = ar_results.params.to_numpy()

ind_covar_ests[region] = ar_results.cov_params().to_numpy()

/home/runner/work/unit-averaging/unit-averaging/docs/examples/plot_1_basics.py:181: PerformanceWarning: DataFrame is highly fragmented. This is usually the result of calling `frame.insert` many times, which has poor performance. Consider joining all columns at once using pd.concat(axis=1) instead. To get a de-fragmented frame, use `newframe = frame.copy()`

german_data["Germany_lag"] = german_data["Deutschland"].shift(1)

Note

This unit-averaging package is designed to accommodate a variety

of packages for estimating the unit-level models.

Focus Function¶

With the model in hand and estimates in hand, we need to express the target parameter (unemployment for Frankfurt in 01.2020) as a function of the parameters of the unit-level models. Mathematically, the model implies the following forecast function:

The function \(\mu\) is called a focus function. It is the bridge between unit-specific estimates and the target parameter. It defines how to combine the estimated coefficients (e.g., \(c_i, \alpha_i, \beta_i\)) into a single forecast (e.g., Frankfurt’s unemployment change).

In general, the package offers two classes for defining a focus function:

an InlineFocusFunction or implementing a concrete

BaseFocusFunction. The former option is convenient when \(\mu\)

and its gradient are already available in form of callables or a simple lambda

function. These are then simply passed as arguments to the constructor of

InlineFocusFunction. The latter option is more flexible and requires

implementing the focus function and its gradient as methods.

In our case, the focus function and its gradient are relatively simple, so we

use an InlineFocusFunction. We pass suitable lambda functions as the

focus_function and gradient arguments:

# Extract data on last month of target region

target_data = (

german_data.loc["2019-12", ["Frankfurt", "Germany_lag"]].to_numpy().squeeze()

)

# Construct focus function

forecast_frankfurt_jan_2020 = InlineFocusFunction(

focus_function=lambda coef: (

coef[0] + coef[1] * target_data[0] + coef[2] * target_data[1]

),

gradient=lambda coef: np.array([1, target_data[0], target_data[1]]),

)

Using Optimal Unit Averaging¶

Defining and Fitting the Averager¶

We are now in a position to create and fit our OptimalUnitAverager. As

inputs, we pass our focus function, the individual-level estimated coefficients,

and the individual-level coefficient covariances:

averager = OptimalUnitAverager(

focus_function=forecast_frankfurt_jan_2020,

ind_estimates=ind_estimates,

ind_covar_ests=ind_covar_ests,

)

To fit any averager in this package, we call the fit() method and supply

the ID of the target unit. If the ind_estimates is a dict, the target unit

is identified by the corresponding key. If ind_estimates is an array, one uses

the index of the unit. We are in the former case:

averager.fit(target_id="Frankfurt")

See also

We are using the OptimalUnitAverager in the conceptually simpler

agnostic (“fixed-N”) regime. OptimalUnitAverager can also make

use of prior information (“large-N”) regime. See

this tutorial for using the large-N

regime.

Tip

The averager classes of this package follow a two layer approach which separate the unit-level estimates from the focus transformation. This allows one to consider several focus functions on the same dataset. However, one may also directly supply precomputed target parameters, and pass an IdentityFocusFunction if that is more convenient in a given context.

Results¶

Calling fit() on averager object makes it compute the averaging weights

and use them to compute the averaging estimate for the specified focus parameter.

These values are stored in the weights and estimates attributes,

respectively. We now take a brief look at each of the two.

Weights¶

We start with the weights. The computed weights are stored as NumPy arrays in

the weights attribute:

print(averager.weights[:10].round(3))

[0.011 0.008 0.008 0. 0.005 0.01 0.024 0.004 0.009 0. ]

The keys attribute maps weights to their corresponding regions:

print(averager.keys[:10])

['Aachen - Düren' 'Aalen' 'Ahlen - Münster' 'Annaberg-Buchholz'

'Ansbach - Weißenburg' 'Aschaffenburg' 'Augsburg' 'Bad Hersfeld - Fulda'

'Bad Homburg' 'Bad Kreuznach']

One may easily create a dictionary of weights by combining the two attributes:

weight_dict = {}

for key, val in zip(averager.keys, averager.weights, strict=True):

weight_dict[key] = val

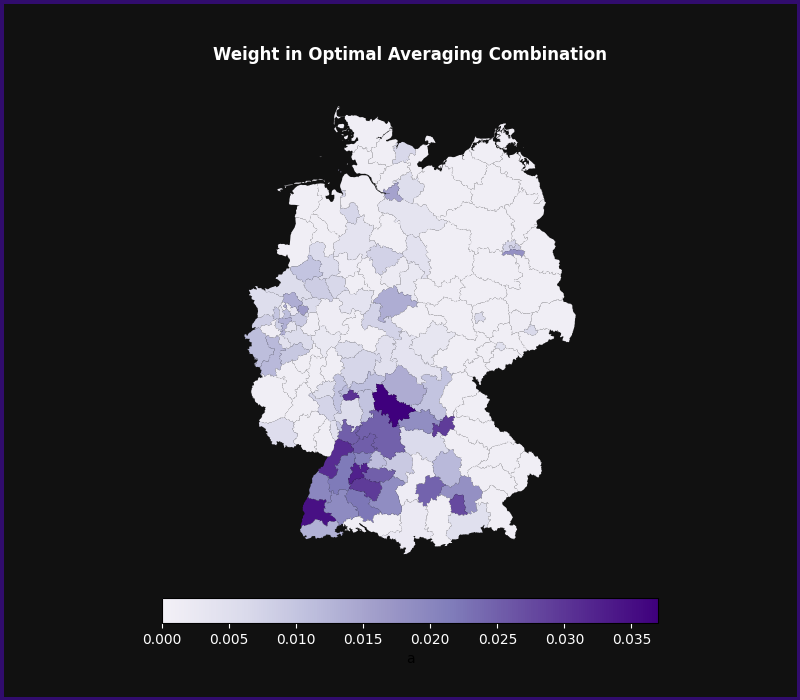

These weights may themselves then be analyzed for patterns. For example, we may plot the weights assigned to each region when computing the optimal combination for Frankfurt:

weight_df = pd.Series(weight_dict).reset_index()

weight_df.columns = ["aab", "weights"]

fig, ax = plot_germany(

weight_df,

"Weight in Optimal Averaging Combination",

cmap="Purples",

vmin=-0.005,

)

This map shows how the averaging estimator assigns weights to improve the quality of the forecast for Frankfurt. As we can see, relatively large weights are assigned to Frankfurt itself (broadly in the middle of the country), and the regions surrounding it. Hamburg (in the north), Munich (southeast), Berlin (east), and the Rhein-Ruhr region (west) also receive some weight.

Averaging Estimate¶

We now turn to the averaging estimates themselves. The estimated value of the

target parameter (unemployment in Frankfurt) is stored in the estimate

attribute:

print(averager.estimate.round(3))

-0.115

In other words, the optimally weighted forecast is that of a 0.11% decrease in the unemployment rate in the region.

We can easily compare that forecast with a forecast without any unit averaging

and simply using Frankfurt-only data. IndividualUnitAverager is a convenience

class that implements using target-unit only data with the same interface

as other averagers:

ind_averager = IndividualUnitAverager(

focus_function=forecast_frankfurt_jan_2020,

ind_estimates=ind_estimates,

)

ind_averager.fit(target_id="Frankfurt")

print(ind_averager.estimate.round(3))

-0.115

In this case the individual forecast is close to the averaged one. Assuming that the individual forecast is broadly unbiased, this means that the averaged one will have lower variance due to using data on more regions.

Finally, every averager in the package (and any custom averager that inherits from

BaseUnitAverager) also implements an average() method that allows one

to reuse the fitted weights with a different focus function.

As a very simple example, we can define a forecaster for some other time point, say, for 12.2019:

other_target_data = (

german_data.loc["2019-11", ["Frankfurt", "Germany_lag"]].to_numpy().squeeze()

)

other_focus_function = InlineFocusFunction(

focus_function=lambda coef: (

coef[0] + coef[1] * other_target_data[0] + coef[2] * other_target_data[1]

),

gradient=lambda coef: np.array([1, other_target_data[0], other_target_data[1]]),

)

We now pass the new focus function to the average() method:

averager.average(other_focus_function).round(3)

np.float64(-0.02)

Tip

It is best practice to refit weights for every focus

function separately, since that allows the averager to optimally exploit

the relevant similarities in the data. Reusing weights average()

is only recommended with similar focus functions or when computation

is expensive.