Different people react differently to same change in \(\bx\)

Average effect of going from \(\bx_1\) to \(\bx_2\) is \((\bx_2-\bx_1)'\E[\bbeta_i]\)

Want to learn \(\E[\bbeta_i]\)

Issue with FE Estimators and This Lecture

Last time proved that under model (1) FE estimators estimate weighted average \[

\hat{\bbeta}^{FE} \xrightarrow{p} \E[\bW(\tilde{\bX}_i)\bbeta_i]

\] Outside of RCTs usually \(\E[\bW(\tilde{\bX}_i)\bbeta_i]\neq \E[\bbeta_i]\)

Weights \(\bW(\cdot)\) “nice”: positive definite and integrate to 1

But \(\bW(\cdot)\) — difficult to interpret

This lecture — way to estimate \(\E[\bbeta_i]\) with panel data

Empirical Motivation

Last time discussed relationship between pollution and labor market outcomes using US county-level data

What if pollution effect differs between counties?

E.g. due to different population characteristics (age, health, …)

Would be an example of model (1). FE estimate from last time would be \(\E[\bW(\tilde{\bX})\bbeta_i]\)

What is \(\E[\bbeta_i]\)?

Theory

Construction

Model and Data

Vector form of realized outcomes in model (1): \[

\bY_i = \bX_i\bbeta_i + \bU_i

\]\(\bbeta_i\) — \(p\)-vector. Interested in \(\E[\bbeta_i]\)

Assumption: \(T\geq p\)

At least as many observations as there are coefficients

Last time assumed that two random intercepts sufficient to capture important unobserved components:

County-season

State-year

Unit of analysis effectively county in given season (e.g. King County in summer is a single \(i\))

After that assumed that effect of pollution was same between places

Allowing Different Effects

What if pollution effects differ between counties and seasons?

Specify model as example of (1) \[ \small

Y_{it}^{\bx} = \alpha_i + \beta_i\text{Smoke Days}_{it} + \text{State-Year FE} + U_{it}

\]\(i\) — county in given season; \(t\) — years

Keep state-year effect to capture “global” effects

\(\E[\beta_i]\) — object of interest

Estimation and Results

Estimation Steps

Our approach to estimating with \(\E[\beta_i]\) with mean group estimator:

Eliminate state-year FE

Compute all individual effects

Compute MG estimator

Step (1) not part of MG estimation, included here due to our model

Eliminating State-Year FE

How do we eliminate state-year random intercept?

One-way within transformation:

Average inside each (state-year)

Take out that average from \(Y_{it}\) and \(X_{it}\)

Loading, preparing data. Eliminating state-year random intercepts

Mean group not implemented anywhere (to the best of my knowledge), but very easy to do by hand

With a for-loop

By grouping the data based on county-quarter ID

A small function for running individual regressions:

Function for running unit-level OLS

def run_individual_regression(county_quarter_df: pd.DataFrame) -> np.float64:""" Compute the OLS coefficient for 'smoke_days_no_state_year' on 'diff_payroll' for a given county-quarter DataFrame. Parameters ---------- county_quarter_df : pd.DataFrame DataFrame containing at least the columns 'diff_payroll' and 'smoke_days_no_state_year'. Returns ------- np.float64 Estimated coefficient for 'smoke_days_no_state_year'. Raises ------ KeyError If required columns are missing. ValueError If regression cannot be performed (e.g., insufficient data). """try: y = county_quarter_df['diff_payroll_no_state_year'] X = sm.add_constant(county_quarter_df['smoke_days_no_state_year']) model = sm.OLS(y, X) results = model.fit() coef = results.params['smoke_days_no_state_year']return coefexceptKeyErroras e: # Column missingraiseValueError(f"Required column missing: {e}")exceptValueErroras e: # Regression-related issuesraiseValueError(f"Regression could not be performed: {e}")

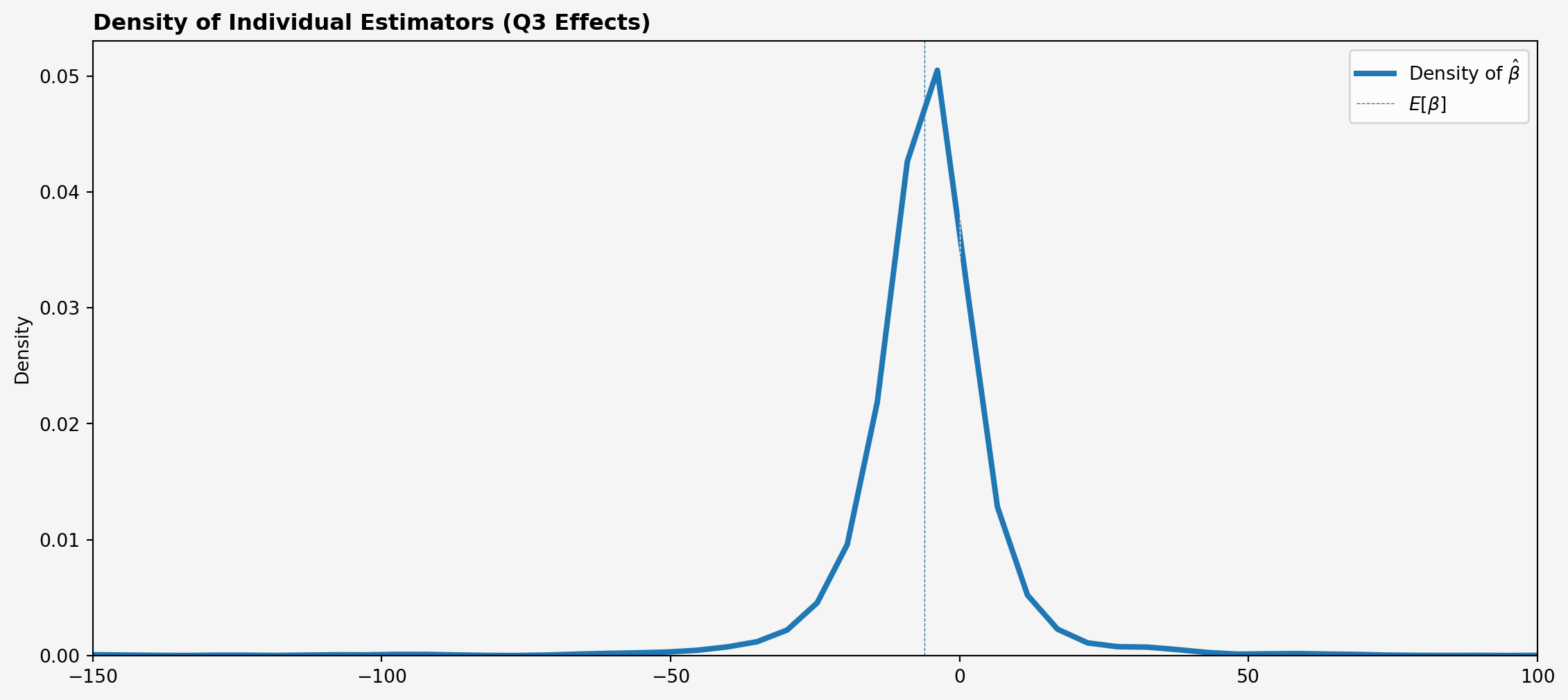

Large standard deviation! Cannot reject \(\E[\beta_i]=0\) — do not have the finding of Borgschulte, Molitor, and Zou (2024) in this model

Visualizing Density of \(\hat{\beta}_i\)

Why Such a Large Standard Deviation?

Density of \(\hat{\beta}_i\) wide, could be due to two reasons:

Large \(\var(\beta_i)\). Means \(\E[\beta_i]\) would be difficult to estimate even without estimation noise

Large \(\var((\bX_i'\bX_i)^{-1}\bX_i'\bU_i)\) — estimation noise dominates

In first case collecting more \(T\) would not help

Visualizing Geography of Effects

Recap and Conclusions

Recap

In this lecture we

Proposed the mean group estimator as an approach to estimating \(\E[\bbeta_i]\)

Discussed its asymptotic properties

Next Questions

What if we don’t care about causal parameters and only want to predict outcomes?

When does strict exogeneity fail? What is the impact of that failure?

How to work with panel data in nonlinear settings?

References

Borgschulte, Mark, David Molitor, and Eric Yongchen Zou. 2024. “Air Pollution and the Labor Market: Evidence from Wildfire Smoke.”Review of Economics and Statistics 106 (6): 1558–75. https://doi.org/10.1162/rest_a_01243.

Morozov, Vladislav. 2025. “Econometrics with Unobserved Heterogeneity.”Econometrics with Unobserved Heterogeneity. https://zenodo.org/doi/10.5281/zenodo.15459848. https://doi.org/10.5281/ZENODO.15459848.